Production continues to climb Steel prices fear to remain weak

Production has continued to climb, and steel mills have not seen a drop in production. Although inventory has continued to decline, it is still higher than in previous years. At the same time, steel demand in June entered the off-season. The pattern of overall oversupply in the steel market cannot be improved in the coming month. Under such circumstances, the steel price may remain weak.

Production has continued to climb, and steel mills have not seen a drop in production. Although inventory has continued to decline, it is still higher than in previous years. At the same time, steel demand in June entered the off-season. The pattern of overall oversupply in the steel market cannot be improved in the coming month. Under such circumstances, the steel price may remain weak. At the same time, the macroeconomic aspect is still weak, and it is difficult for the government to introduce major stimulus policies at the policy level. In this case, funds will remain cautious about risky assets.

Although the price of course has fallen relatively deep from the highs at the beginning of the year, many entrants are also eager to try. We do not rule out a technical rebound in the price of money driven by funds, but we still maintain the view of the mid-term bearish steel price.

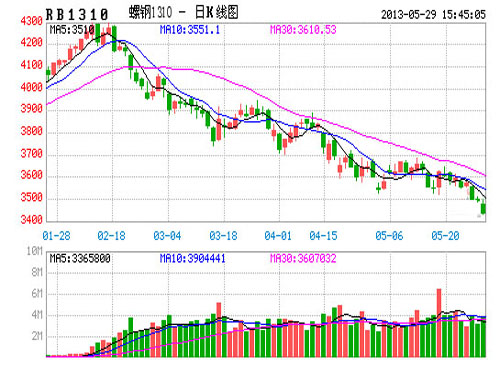

Review of the first part of the market price thread prices in May remained at a low level of shocks, both long and short sides in the 3500-3700 within a small range of sustained tug of war, the level of market positions also continued to increase, on May 16 reached a record 1976540 hand, and previous thread The highest position record was 1971454 on September 5th, 1212. As of May 24th, the position of the thread was 1,771,476 lots, which was still nearly 390,000 lots higher than 1,387,116 at the end of April.

The large amount of open positions shows the market's disagreement on the trend of thread prices. On the one hand, the overall supply and demand pattern of steel has not been improved, and trend traders continue to look into the market. On the other hand: After experiencing more than three months of decline, the current price level is not far from last year's low level. The funds were just around the corner and there was an urge to grab the bottom, especially if many varieties had already experienced low rebound.

On the whole, the price of the thread during the month of May was still in a weak process, and the trend of market decline has not been reversed.

Part II Fundamental Analysis 1. The economic situation has weakened and the market risk appetite has been difficult to increase. The market originally thought that the domestic macroeconomic situation would experience a seasonal pick-up after entering the second quarter. However, the National Bureau of Statistics released the April economic data. No imaginative optimism.

In April, the year-on-year growth in fixed asset investment fell slightly to 20.1%. The declining growth rate of infrastructure investment dragged down the overall investment slowdown, especially investment in water conservancy and environmental protection and public utilities (1708.301, 11.88, 0.70%). The growth rate of manufacturing investment continued to fall after recovering in March.

Although the year-on-year growth rate of industrial added value rebounded from 8.9% in March to 9.3%, it was mainly due to the base effect. Although statistics from the Bureau of Statistics show a strong rebound in industrial production from the previous quarter, this is more due to the base effect. In fact, compared with the market's expected 9.5% level, 9.3%% is still low.

The macroeconomic weakness has not changed, the market's risk appetite continues to decline, and risky assets are hardly favored by investors in the short term.

Second, production continues to create "Chinese records"

In the first half of April, the average daily crude steel production reached 2.12 million tons. The subsequent domestic crude steel production continued its growth trend. In the first half of May, the average daily average crude steel output again set a new record, reaching a record high of 2.193 million tons. In the same period last year, it was 150,000 tons (2.04 million tons in the same period last year was also the highest in the year).

It is clear that the declining steel prices have not affected the enthusiasm of the steel mills. This is mainly due to the fact that prices of raw materials including iron ore and coke were lower than the same period of last year, and the gross profit per ton of steel was not as bad as last year's level. In addition, it is still in a seasonal peak season in May. Steel mills have higher expectations for the later period.

For the 2.19 million tons of average daily crude steel production, we have two points of understanding:

First, this production level may be the highest level this year for two reasons: First, according to past practice, the annual May is often the time when the output is highest in the year. In addition, from the mid-term, we see the start of the domestic blast furnace utilization rate. There is a slight decline, which will affect the production of crude steel in the later period.

Second, there will not be a rapid drop in crude steel production. From May 20th, the Tangshan area began to implement measures such as blackouts and dismantling of equipment in blast furnaces that did not meet the standards. However, from the viewpoint of the current blast furnaces to be demolished, most of them have been discontinued and do not affect the production of crude steel in the later period. From the rest of the country, the profit and loss situation of steel mills has not yet reached the boundary conditions that led to their large-scale production cuts.

Third, the real estate market exceeded our expectations. We originally thought that many homebuyers would finish their transactions before the five state regulations were completed in March. Real estate sales will slow down significantly in April. However, in fact, the sales area in April increased by 40% year-on-year, and the growth rate was much higher than the 27% in March.

Affected by the introduction of the State’s five regulations, the area of ​​new housing starts in March fell by 20% year-on-year. From the current situation, it seems that developers have overreacted to the introduction of the five countries. With local governments downplaying regulations, the central government did not exert further pressure. Openers re-intensified their efforts to start construction. The area of ​​newly started construction in April rebounded to 14.5% year-on-year.

The speed of new start-ups has increased real estate investment. In April, domestic growth was 23% year-on-year, the highest growth rate in the past four months.

It is expected that the real estate policy will remain stable in the next few months and the real estate market will continue its moderate recovery.

Fourth, raw material prices continued to slump In July 12 years after the domestic port iron ore increased to 100 million tons, stocks began to appear more than 9 months of destocking. However, recently, its inventory seems to have stabilized. The data from Xiben shows that the inventory of iron ore ports has increased continuously for four weeks, ending at 7.610 million tons as of May 24, but still 21 million tons lower than the same period of last year. .

The market originally hoped that the low level of inventory will increase the support for ore prices. With the increase in stocks, this expectation will be lost. Affected by the falling prices of finished steel products (3464, 33.00, 0.96%) and the increase in port ore prices, the price of imported ores has fallen below 130. As of May 23, the Platts index was $123, a decrease of $10.75 from the end of last month. The current price is the lowest price in mid-December of the previous year.

Relative to the market trend of finished steel prices, the billet price performance is even weaker, although the billet inventory declines quickly. The inventory of Tangshan billet fell from 1.97 million tons in mid-March to the current 990,000 tons.

The quick inventory did not prevent the drop in billet prices because banks strengthened the supervision of billet pledges, market capital tightening, and billet palletizers were affected.

With the fall of ore prices, the production cost of rebar has also rapidly declined. As of May 24, the production cost of domestic mainstream rebar was 3,517 yuan/ton, which was a decrease of 140 yuan/ton from the end of last month.

5. Social inventory and steel mill inventory performance varied. Social inventories continued to decline in May. As of May 24, the domestic steel (3464, 33.00, 0.96%) social inventory was 18.61 million tons, down 620,000 tons from the end of last month. This was the tenth week after the social inventory reached 22.5 million tons in mid-March. However, the current social inventory is still 2.82 million tons higher than the same period last year.

From the perspective of different varieties, rebar was 1.45 million tons higher than the same period of last year, and wire rod (3560, -18.00, -0.50%) was 510,000 tons higher than the same period of last year. Hot-rolled steel was 860,000 tons higher than the same period of last year, while cold-rolled steel The board declined slightly from the same period last year.

With the return of the temperature, the demand for steel products will slow down. In particular, the demand for construction steel will be off-season in the short-term and the late-stage traders will be de-stocking, which means that the social inventory will continue to decline.

Unlike the continuous decline in social stocks, steel mills' stocks have increased from time to time. As of the end of May, the inventory of steel mills was 13.09 million tons. Although it was lower than the 14.51 million tons in mid-March, it was still at a high level. Compared with the 11.22 million tons in the same period of last year, the inventory of current steel plants was 1.87 million tons higher. It is difficult for steel mill stocks to show a downward trend of social stocks, mainly due to the large output of steel mills.

With the end of the peak season, if the steel mills maintain their current production levels, there will be a possibility that the latter steel stocks will rise. The increase in steel stocks will force it to lower its ex-factory prices.

The third part of the market outlook First, the market outlook, the output is continuing to climb, while the steel mills are not seeing production cuts; while inventory continues to decline, but still higher than in previous years levels. At the same time, steel demand in June entered the off-season. The pattern of overall oversupply in the steel market cannot be improved in the coming month. Under such circumstances, the steel price may remain weak.

At the same time, the macroeconomic aspect is still weak, and it is difficult for the government to introduce major stimulus policies at the policy level. In this case, funds will remain cautious about risky assets.

CHANGZHOU ANTALYA TOOL AND MACHINERY CO., LTD. , https://www.atly-tool.com